The effect of Chinese stock market gyrations on the real economy could be less than feared

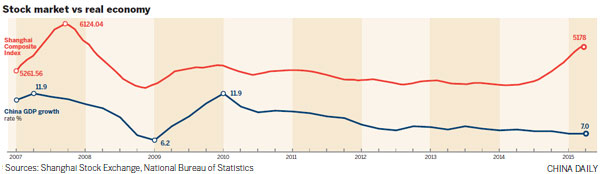

The Shanghai Composite Index suffered its worst daily fall in eight years - nearly 8.5 percent - on July 27, which sent shockwaves through other markets around the world.

Values have since continued on a roller-coaster ride, and it is now the impact of this turbulence on the Chinese economy that is now causing the most concern.

With this degree of volatility, some ask whether the Chinese government will be able to maintain its target of about 7 percent growth this year

Certainly, if these falls had been experienced on many of the leading bourses around the world, economists would be expecting some consequent fall-off in economic performance.

This is because stock markets are often the main engine of market economies.

The market capitalization of China's two main exchanges, in Shanghai and Shenzhen, was 55.84 trillion yuan ($12.54 trillion; 8.27 trillion euros) at the close on July 24, nearly 88 percent of China's 63.64 trillion yuan GDP in 2014.

Yet the value of shares available for trading on the exchange was, by most estimates, just 35 percent of GDP compared to many international exchanges, where the shares traded exceed that of the host country's GDP.

Many of the listed companies in China are, in fact, state-owned enterprises with large government shareholdings - only 29 percent of the shares of China's biggest listed company, Industrial and Commercial Bank of China, are available for trade, according to Bloomberg Data.

Furthermore, just 8.5 percent of household assets (not including property) were invested in shares in China compared to 63 percent held in cash on deposit at the end of 2013, the latest available data, according to the People's Bank of China.

With 46 million new share accounts being opened in the second quarter of this year, most estimates suggest this figure may have doubled to 15 percent, but it still implies the wealth effects of any falls will have a marginal impact on domestic consumption and, therefore, the economy.

The recent turbulence in the stock market therefore may not have any dramatic effect on the wider economy.

Despite the recent upheaval, the market also remains substantially up from when it began to surge in the middle of last year.

Paul Gillis, professor of accounting at Guanghua School of Management at Peking University, who was speaking from Silicon Valley, says it would be wrong to assume China was experiencing some 1929 Wall Street Crash moment.

"I think China's markets are still far too immature to have such a big impact on the wider economy. With 1929 there was a bubble that pushed the US into a long depression and the then government response was pretty weak," he says.

"The big difference is that the Chinese government is going to take action to make sure there isn't any contagion effect. I think the real point here is we are seeing a very necessary correction. The valuations on stocks were just not justifiable."

Dariusz Kowalczyk, senior economist and strategist with Credit Agricole Corporate and Investment Bank, based in Hong Kong, also believes that the Chinese stock markets and the real economy operate in almost parallel universes.

"Absolutely, I agree with that big picture. The economic implications of stock market behavior will not be as big as in some other countries that rely on equities to a larger degree," he says.

"I think regardless of what happens to the equity market in the near to medium term, the government has the financial resources over the next couple of years to control the economy and ensure it slows only moderately and does not go through a crash."

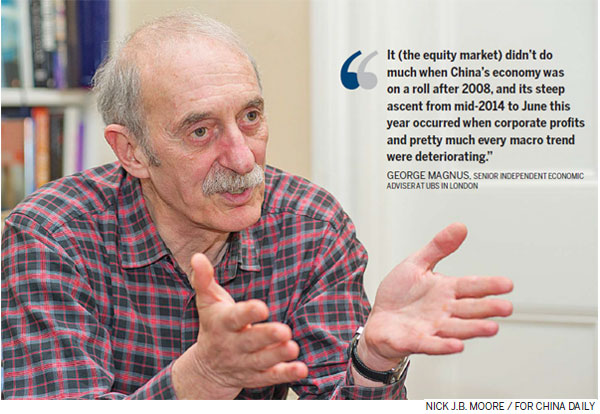

George Magnus, senior independent economic adviser at UBS in London, also does not consider there will be a lasting effect from the recent helter-skelter activity on the markets.

"The equity market isn't really a market, as we commonly understand it in financial markets. It didn't do much when China's economy was on a roll after 2008, and its steep ascent from mid-2014 to June this year occurred when corporate profits and pretty much every macro trend were deteriorating."

Research by Goldman Sachs suggests there is very little correlation between the performance of any country's stock markets and its economy and that nowhere has that been more true than in China.

It points out that China's economy has outgrown that of the US by 8 percent a year since 1992 but its equity market has lagged behind that of the US by 8 percent a year - an almost perfect negative correlation.

John Ross, senior fellow at Chongyang Institute for Financial Studies, Renmin University of China, says this is not just the pattern in China but everywhere.

"The faster an economy grows the worse its stock market does over the longer term. There is, in fact, this negative correlation. This is not just the result of one study but all studies," he says.

"Over the shorter term, there tends to be more of a positive correlation, but in China the share market is so peripheral to China's economy. It is a bit like a feather floating around in the air, compared to the effects of interest rate cuts and reserve requirement ratio shifts."

Zhu Ning, deputy director of the Shanghai Advanced Institute of Finance and one of China's most respected finance experts, does not believe there is anything to be celebrated about the stock market and the economy not being in tandem, if that is the case.

"If share prices are totally unrelated to the Chinese economy, then what that tells is that the Chinese stock market is a failure, purely a gambling market, rather than based on information. There really ought to be some connection," he says.

Zhu thinks the emergency measures the Chinese government has taken to stabilize the market over the past few weeks such as limiting short selling, banning margin trading (borrowing money to buy shares), direct stock purchases and emergency interest rate cuts, send the wrong message.

"I think attempts to sway the market set a very bad example. What investors learn from this is that the government is going to bail them out. They are going to take even more irresponsible risks in the future."

One pressure on the economy from the recent stock market falls could be the damage done to the country's financial services sector.

Somewhat under the radar, it has become a significant driver of China's GDP, particularly over the past few months.

In the first half of this year, when the Shanghai Composite Index was roaring ahead, the financial services sector grew at 19 percent year-on-year.

This was almost three times the growth of the overall economy and a marked increase on the 11 percent the sector grew in the first half of 2014.

Kowalczyk at Credit Agricole CIB, says that if financial services had not grown so fast then the government would have missed its 7 percent growth target.

"If the sector had grown at the same rate of the first half of last year at 11 percent, the overall economy would have grown by 6.3 percent and not 7 percent. It is therefore fair to assume that in the second half of this year, financial services won't be making this outsize contribution to growth."

Zhu at the Shanghai Advanced Institute of Finance insists also that it is wrong to dismiss out of hand the importance of the stock market to the rest of the economy just because its traded shares represent a relatively small proportion of GDP.

He says this understates the role the share market is now playing in funding companies right from recent IPO listings, of which there have recently been record numbers, right up to the major state-owned enterprises.

"Other sources of funding such as shadow banking vehicles have largely dried up over the past two to three years. China does not have any sort of developed bond market either, so the stock market has become very much a primary source of revenue for many companies. This is very different from the West, where there is an array of sophisticated financing sources," he says.

"Over the past six months, the stock market has been a very cheap and easy place to raise money since companies have enjoyed having twice the share price valuation they had previously without generating any additional revenues or profits."

One way the stock market falls could have an effect on the economy is if there is a wealth effect on consumption.

Some 70 percent of those who invest on the China exchanges are private individuals, which is in marked contrast to exchanges in London and New York, which are dominated by institutional investors.

Millions have invested small fortunes, hoping for quick returns, and in recent days many of these will have been feeling a lot poorer and therefore less likely to want to spend.

Yet despite this frenzy, only 6.8 percent of urban households in China have stock accounts and 70 percent of these accounts had less than 100,000 yuan in them.

Oliver Barron, head of the China office of NSBO, which provides research on the Chinese economy, says there has to be a sense of proportion about recent events.

"The declines in share values do not necessarily mean the destruction of wealth for all households," he says.

"It will surely dent consumer confidence and may have a notable impact on retail sales in July and August but the impact is unlikely to be lasting."

Kowalczyk, however, thinks there could be some impact on consumption, which could ultimately impact on growth.

"If you look at the second quarter data, consumption accelerated quite sharply and was one of the key reasons why growth overall was quite stable. There is a risk that this could be undermined by the negative wealth effect from the stock market."

If the stock market volatility was to impact both on consumption and the contribution of a buoyant financial services sector, then the government might be forced again to hit the investment lever and pour money into infrastructure investment to achieve its growth target.

The risk would be further increases in local government debt, which is seen as one of the key weaknesses of the economy.

It was revealed on July 24 that local government debt had risen to 30.28 trillion yuan at the end of 2014 from 17 trillion yuan in the middle of 2013 when the Chinese Academy of Social Sciences published the government's balance sheet.

So far from having a minimal effect on the economy, the stock market volatility could effectively mean the government putting on hold its still nascent attempts to rebalance the economy away from investment to being more consumption-led on hold.

"Sure, there is a real risk of that," adds Kowalczyk. "If this were the case then there would be major implications to what is currently happening with the markets."

For Zhu at the Shanghai Advanced Institute of Finance, this presents a persuasive case for the government to be more relaxed about the growth target.

"There are going to be calls for a more active fiscal policy and more quantitative easing but I think we have to put things in the right perspective. America is close to 3 percent growth and they are really celebrating. Maybe for China 6 percent is not that bad after all."

Magnus at UBS says the markets drama has implications for the reform agenda generally and might lead the government to tread very carefully.

"I think it is a setback for the government's insistence that it can introduce market forces into essentially a planned economy. Financial reforms were considered the most likely to make rapid headway, but I suspect even this may now be looking a little jaded."

The jitters in China's stock markets have already hit commodity prices with implications for commodity producing nations in Africa and elsewhere.

Slowing China growth had already forced the S&P GSCI commodities index down by 36 percent over the past year. The share price turmoil has seen Brent crude slump to $52.77 a barrel and iron ore fall 11 percent in just one day in early July.

Kowalczyk believes the stock market volatility may actually prove beneficial for commodity prices later in the year.

"It may be something of a paradox, but what is happening with shares does impact on growth and if the government decides to invest in infrastructure, that will lead to increased demand for commodities."

In the meantime, not only Chinese investors but those worried about the global economic outlook are waiting for the current market instability to abate.

The specter for many might not be the Wall Street Crash of 1929, but more like what happened to Japan when its stock market bubble burst at a peak in December 1989, to which it has not returned even 26 years later.

Some analysts have pointed to recent swings in the Shanghai Composite precisely mirroring what happened before the Tokyo crash.

If there was to be an impact on the Chinese economy from the recent volatility that would almost certainly feed back again into the share market.

"I am not predicting any big disaster," says Gillis at Guanghua School of Management. "But if China does plod along at 6 or 7 percent growth over the next few years, that sort of growth is not going to carry the valuations that some of the stocks are currently listed at."

andrewmoody@chinadaily.com.cn

|

Paul Gillis, professor of accounting at Guanghua School of Management at Peking University. |

|

John Ross, senior fellow at Chongyang Institute for Financial Studies, Renmin University of China. |

|

From left: Oliver Barron, head of the China office of NSBO; Zhu Ning, deputy director of the Shanghai Advanced Institute of Finance; Dariusz Kowalczyk, senior economist and strategist with Credit Agricole Corporate and Investment Bank, based in Hong Kong; and Louis Kuijs, chief economist, Greater China, RBS. |

( China Daily Africa Weekly 07/31/2015 page1)

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()