Bogged down by billions in nonperforming loans, lenders outsource recovery to external agencies

Li Wen's voice went hoarse recently, the result of making hundreds of phone calls in the past two months to credit card holders who failed to pay their bills.

For debt collectors like Li, 28, at Shanghai China Promise Ltd, now is a boom time as lenders have seen a sharp increase in the number of bad loans over the past five years.

|

A Marble lion in front of the China Banking Regulatory Commission office. A report by China Orient Asset Management Corp predicts nonperforming loans could continue to grow. Provided to China Daily |

Banks, peer-to-peer lending platforms and microfinance companies across China are giving more business to such agencies, especially in areas where has credit has expanded and economic growth has slowed.

Outsourcing is the cheaper option, according to Chai Jun, a manager at Shanghai Heng Xin Asset Management Co. He says it can cost a branch of a commercial bank more than 3 million yuan ($457,000; 419,000 euros) to employ a full-time team of debt collectors, while outsourcing can cut the cost by more than half.

The need for debt collection agencies is highest toward the end of June and December, the seasonal peaks for lenders scrambling to meet the semi-annual asset quality requirements.

The team at China Promise has grown from 120 members to 500 in the past two years, and the company plans to hire more in the next few years.

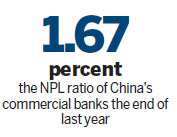

A report by China Orient Asset Management Corp, which manages bad loans, predicts nonperforming loans could continue to grow. By the fourth quarter of last year, the NPL ratio of China's commercial banks was 1.67 percent, up 8 basis points quarter-on-quarter.

The trend started in the second quarter of 2013, according to the China Banking Regulatory Commission. By the end of 2014, commercial banks were staring at more than 35.76 billion yuan in bad credit card debt, up 42 percent year-on-year, show the latest data from the China Banking Association, released in July.

While debt collector Li continues to make phone calls, some of her colleagues are charged with confronting debtors face to face, to urge them to repay. If they refuse, agencies, working in tandem with law firms, can issue legal notices or file lawsuits.

"Everything must be legal and transparent, and every phone call, visit and document is recorded. Otherwise, we'll be no different from hooligans," Li says.

She sees her job as essential to helping build a society with better credit.

Xiao Bo, founder of Zero One Technology Co, a Beijing-based enabler of trading in nonperforming assets, agrees and says: "Debt collectors generally don't adopt violent means. An odd extreme case could involve getting physical with debtors, but that's about it. For debt collection agencies, profits are not so high as to compel them into adopting illegal methods."

However, insiders say lenders such as peer-to-peer lending platforms, small loan companies and guarantee companies are not averse to "taking off the kid gloves" with debtors.

Ye Mingbo, a 24-year-old shop assistant, was contacted by debt collectors in May. He had used his credit card to buy a laptop and camera lenses on installment, but failed to keep up the repayments on his 8,000 yuan bill after losing his job.

After six months, he started receiving text messages from the bank, then phone calls from its credit card services department. Shortly after, he started to receive calls from a debt collection agency. On the fourth call, he says the agency called and gave him advice on how to analyze his financial situation and repay his bill.

Contact the writers at wuyiyao@chinadaily.com.cn and jiangxueqing@chinadaily.com.cn

(China Daily Africa Weekly 03/04/2016 page28)

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()