Sudden drop in RMB a shift toward market-driven rates, not a growth boost, experts say

After several days of turbulence on the foreign exchange markets, the Chinese currency, at least for now, looks to be heading for a period of calm.

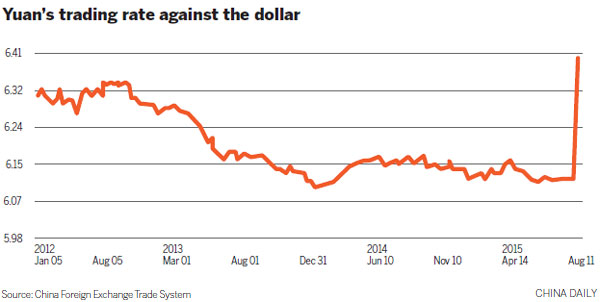

When the People's Bank of China took the decision to let the yuan slide by 1.9 percent on Aug 11 - the biggest daily fall since 1994 - it prompted fears of currency wars and global deflation.

Many also thought the move was designed to boost China's flagging exports so the government hits its 7-percent growth target in the second half.

There was also speculation the government was trying to pre-empt a much-anticipated hike in the US interest rate by the Federal Reserve Bank in September.

Increasingly, the official explanation that the move was a step toward a more market-oriented exchange rate mechanism is gaining acceptance as the most valid.

It has since emerged that the International Monetary Fund and Chinese financial chiefs had reached broad agreement in May that the markets should play a bigger part in setting the value of the yuan.

Just days before the PBOC made its move, the Washington institution also circulated a report among staff members concluding that reform was needed, which many now believe was the final catalyst in the decision that shocked world markets.

Some even believe that as early as November, when the IMF has its next board meeting, it may recommend that the yuan becomes a global reserve currency and joins the dollar, the euro, the UK pound and the yen in the SDR, or special drawing rights, the supplementary foreign exchange reserves held by the IMF.

The yuan would be the first currency to be accepted into the basket since the euro in 1999, and it would be a key step toward becoming a major international currency.

The IMF said in a statement on Aug 19 that if it was to give the green light, the currency would not join the basket until September 2016 at the earliest.

Its managing director Christine Lagarde said in March it was not a question of if the yuan joined the SDR but only when.

Donna Kwok, senior China economist at UBS in Hong Kong, believes this is now a real possibility, despite skepticism in some quarters whether the yuan is ready for such exposure.

"There are essentially two tests for this. One is how much the currency is traded, and the second is whether a currency is freely usable. The problem is everyone focuses on how much China fails the second test without taking into account how much it excels on the first one."

One of the factors behind its inclusion will be whether a more freely floating yuan will be moving in only one direction: downwards.

The move by the PBOC that provoked such excitement was to set the yuan's reference rate to the dollar 1.9 percent lower and create a mechanism whereby it can float by 2 percent in either direction. The rate around which it can float is fixed at the start of trading each day using as a reference the closing rate of the previous day. The exchange rate fell for two further days after the move and was 4.4 percent down by the close on Aug 13, but has since rallied.

The PBOC's chief economist, Ma Jun, made clear in a statement on Aug 16 that it has intended there would be "two-way volatility" and not the one-way traffic the markets seemed to have been assuming.

Despite the support from the IMF for the move, the value of the yuan has been a longstanding area of dispute between the US and China, particularly before US presidential elections. It also comes about a month before Chinese President Xi Jinping meets with US President Barack Obama in Washington in September.

"At least for the moment a lot of panic has dissipated, but it hasn't stopped many people shouting from the rooftops that China is triggering currency wars and global deflation," says George Magnus, an associate at the Oxford University China Centre.

"It only needs Donald Trump to get on his soap box and say the Chinese have been doing this for 10 years and it becomes contentious again."

Duncan Innes-Ker, regional editor for Asia, at the Economist Intelligence Unit, based in London, believes there is substantial scope for the yuan to depreciate.

He says many have overlooked that, while the exchange rate against the US dollar has remained relatively flat, the euro is down by 20 percent against the yuan since January 2014 and down against another SDR currency, the yen, by 15 percent over the same period. He also points out the CNH, the offshore version of the yuan, traded in Hong Kong and Singapore, is around 5 percent lower than the onshore one.

"If you look at where the onshore and the offshore rates are and also take into account that the yuan has appreciated significantly recently then a further depreciation of between 10 and 15 percent over the next few months would not be unexpected."

Kwok at UBS, however, predicts volatility. The rate will fall from 6.39 yuan to the dollar on Aug 18 to around 6.5 yuan at the end of 2015 and then 6.6 yuan at the end of 2016, she says.

"While we are expecting a modest degree of depreciation, we think the trajectory between now and then will not be a straight line because the PBOC has clearly stated it wants to see two-way volatility. It does not want a one-way directional trend," she predicts.

Ambrose Evans-Pritchard, international business editor at The Daily Telegraph in London, insists it is just not in China's interest to play any sort of devaluation card.

He points to a Morgan Stanley study at the end of last year that says Chinese companies had $1.3 trillion (1.16 trillion euros) of short-term debt, some 9 percent of the country's total GDP, in overseas loans, which would be made more difficult to pay back if the currency fell in value.

"It would be dangerous for China to pursue such a course. These companies that have borrowed overseas tend to be the weaker ones that have not been able to get money from the Chinese banking system, so they are quite close to distress anyway. So this would be a particular toxic combination."

Mark Williams, chief Asia economist at Capital Economics, the leading economics consultancy, believes the PBOC making a number of interventions in the market is already evidence it does not want to see any immediate further devaluation.

"The fact that the People's Bank has stepped in since to stem the currency decline tells us that the clamor about currency wars was overblown," he says.

"Our initial take was that this was primarily an effort to make the yuan, on paper at least, much more market-driven. The small devaluation that came with the move was probably welcomed, but not the main goal."

Zhu Ning, deputy dean and professor of finance at the Shanghai Advanced Institute of Finance, however, thinks a certain level of depreciation could be beneficial in the current climate.

"If the government wants to go even looser with its monetary and fiscal stimulus packages, there is always a risk of creating asset bubbles. A depreciation would let some air out of these because foreign capital would be less enthusiastic about plowing money into the Chinese stock market and housing market," he says.

Fears about the yuan and the Chinese economy have caused great nervousness among commodity-producing countries, particularly in Africa.

The Bloomberg commodity price index was already at its lowest in 13 years and fell sharply again with news of the depreciation, from just over 92 on Aug 11 to 88.60 on Aug 20.

Michael Power, a global investment strategist, at Investec Asset Management, based in Cape Town, thinks there has been an overreaction.

"The recent acclimatization of the yuan to a more free-floating status - for that is the essence of what has happened, even though many short-sighted commentators have rather hysterically dubbed it a devaluation - will have some impact on commodities and, especially, oil-exporting African nations, and it will be negative," he says.

Power, though, thinks some African countries will benefit from lower commodity prices.

"There are actually more oil-importing countries in Africa than exporting ones, which is often overlooked."

One of the major reasons why there was such a huge global reaction to China's move was that it was seen as an emergency measure to revive the economy.

Factory output figures and retail sales have been disappointing. In July, exports fell year-on-year by 8 percent.

The move was seen as an attempt to boosts exports, as one lever in the government's attempt to meet its 7-percent GDP growth target.

Evans-Pritchard thinks this explanation never actually made sense.

"They never really needed to resort to using the currency for this end. The reserve requirement rate is just 18.5 percent at the moment, and they could bring that right down to single figures if they want to. Only when that gets into single figures am I going to get worried they would be playing their last card."

Many believe the stimulus measures the government have so far put in place - regardless of the exchange rate move - are enough to deliver targeted growth in the second half.

These have included four separate cuts in interests rates, reduction of the RRR, supplementary lending to the banking system, and the sanctioning of up to 1 trillion yuan ($156 billion; 141 billion euros) in the issuance of bonds for local governments to finance debt.

Magnus, at Oxford University, believes these measures add up to about 1.5 percent of GDP.

"I think this suggests the underlying growth of the China economy is now at around 5.5 percent."

With the potential of a depreciating currency, the big risk for China is capital outflows.

Analysis by the Financial Times, published on Aug 18, that net capital outflows of 19 emerging market economies, of which China was the most significant, had reached $940 billion in the 13 months to the end of July led to heavy falls on the Shanghai Composite.

Evans-Pritchard says the pace of outflows in China would accelerate if there was a view the yuan was going to depreciate.

"If there was a perception the government was deliberately driving down the value of the yuan as a long-term policy, this could accelerate out of control and they would have to drain their reserves to defend the currency," he says.

"By doing so they would automatically tighten domestic monetary policy which carries the risk of creating a credit crunch."

With China already a huge economy, many believe the government has no option but to prepare its currency to join the SDR and become a global reserve currency

Williams at Capital Economics says such a status for a currency is no panacea and brings with it responsibilities it may prefer not to have.

"It's not obvious that having a global reserve currency in itself does a country any good - in fact, countries such as Germany and Japan in the past tried to stop their currencies being used internationally because they feared it would cause them to appreciate and hurt their export sectors."

He believes, however, it could be a useful discipline for China in its current state of development.

"In pushing to achieve reserve currency status, policymakers would have to push through reforms to financial markets, making them more open and transparent, that over the long run would deliver benefits to China's economy," he says.

The move on the yuan has already opened another debate on when China's capital markets will be fully open, which would require full convertibility of the yuan. HSBC has predicted this may happen as early as 2020.

Candy Ho, managing director and global head of RMB business development and markets at HSBC in Hong Kong, contends the move is consistent with that.

"With the PBOC also signaling further foreign exchange reforms, such as the extension of the Chinese yuan trading hours and promoting convergence between the onshore and offshore exchange rates, it is clear that China is committed to making the RMB fully convertible sooner rather than later."

Innes-Ker at the EIU believes it is wrong to expect something dramatic.

"This is not the sort of thing where you wake up one morning and suddenly you are there. It is a much more gradual process," he adds

He believes important initiatives have been the Stock Connect Scheme, creating a trading link between Hong Kong and Shanghai and making it easier for foreigners to buy Chinese shares, and he anticipates a further extension of the QFII, or Qualified Foreign Institutional Investor, a quota program that facilitates currency movements in and out of the country.

"This latest move on currency could be another of those key steps."

andrewmoody@chinadaily.com.cn

(China Daily Africa Weekly 08/21/2015 page1)

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()