Policymakers will not allow currency to drop too much because that stymies greater international use

On Aug 11, China announced it was depreciating the yuan by nearly 2 percent. The central bank described the devaluation as a one-off, as it also gave details of a new way of managing the exchange rate that allows the market to play a bigger role in the decision of the reference rate of the yuan.

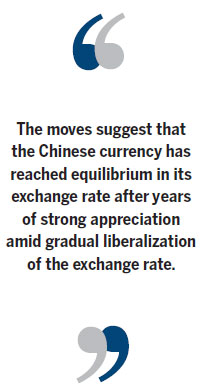

The moves suggest that the Chinese currency has reached equilibrium in its exchange rate after years of strong appreciation amid gradual liberalization of the exchange rate. The currency - barring minor fluctuations - remained flat against the US dollar in the first half of the year, rising by only 0.09 percent.

Looking ahead, the exchange rate is likely to depreciate against the greenback amid changes in economic trends in both the Chinese and the global economies, but the depreciation would be gradual to ensure that the currency would remain stable in general terms.

However, the ratio of trade surplus to the GDP, a major gauge of the fairness of a country's foreign exchange rate, declined after reaching a peak of 10 percent in 2007. The ratio stood at 2.1 percent in 2014, well below the internationally recognized balance line of 4 percent. At the same time, the gap in outbound and inbound investment narrowed. In 2014, the difference was only $16.7 billion (15.1 billion euros); and it is expected that ODI will surpass FDI for the first time this year, leading to a net capital outflow in China's investment account.

Another development that will accelerate capital outflows is the expectation of interest rate increases in the United States. With its economy recovering slowly but steadily, the US Federal Reserve is more than likely to abandon loosening policies .

The market now appears to believe the US central bank will increase the interest rate in September, the first time since the global financial crisis. Although the timing of the rate hike may be uncertain, it is certain that the US will embrace monetary tightening. This will definitely bolster the trend of international capital migrating from emerging markets, including China, to the US.

Consequently, China's net capital inflows will slow, if not decrease, creating the possibility of a drop in value.

The other factor that has bolstered a strong yuan is the Chinese government's keenness to internationalize the currency. Since 2008, Beijing has stepped up efforts to promote the use of the yuan as a settlement, investment and foreign exchange unit across the Chinese border. But given the little recognition in the international market at the initial stages of its internationalization, the government had to allow the yuan to strengthen rapidly to attract overseas people and businesses to use the currency since investors tend to hold currencies whose value is on an upward trajectory.

This tactic paid off in the recent years, with the yuan now the world's fifth-most traded currency internationally.

However, it has also become clear that the marginal effect of a rising yuan has been decreasing, since the overseas market share of the yuan has stabilized at the current level in the past few months. This means that China will need to use other means, such as capital account liberalization, expanded overseas investment and foreign exchange deregulation, to boost the overseas presence of the yuan.

In this sense, the need for the yuan to appreciate to help push for the internationalization of the currency is not as urgent as before.

While the fundamentals for yuan appreciation are weakening, the need for the currency to depreciate is rising.

The first will be the need to spur exports amid a slowing economy. As one of the three traditional growth engines, China's foreign trade registered lackluster performance this year. Total trade dropped 6.9 percent year-on-year to 11.53 trillion yuan ($1.9 trillion) in the first half, according to the General Administration of Customs. Exports rose slightly by 0.9 percent from a year ago to 6.57 trillion yuan, while imports fell 15.5 percent to 4.96 trillion yuan.

Given the first-half performance, it is almost certain China will miss the annual goal of 6 percent growth in foreign trade. It is no surprise the government is eager to spur exports by all means. Therefore, the probability of the yuan appreciating is low.

In the monetary environment, continued loosening also backs a depreciating currency. With the need to bolster the stock market and the overall economy, China will continue to loosen monetary policies by cutting interest rates and injecting liquidity. The supply of the yuan will thus grow, pulling down the yuan's value.

Externally, there are a few factors that provide the conditions for the yuan to appreciate.

Major economies including the European Union and Japan are in a monetary loosening circle with their currencies at a low level. Amid this broad trend, it is natural for the Chinese yuan to follow suit if policymakers deem depreciation is necessary.

In May, the International Monetary Fund said in a report that China's currency was "no longer undervalued", marking a significant shift after more than a decade of criticism of its value. With this change in international attitudes, the pressure on China to continue strengthening the yuan is at its lowest level in at least a decade. So it is possible that China may leverage this amiable international atmosphere to drop the yuan's value to fend off any deeper economic slowdown.

Given all these factors, it is fair to conclude that the continual appreciation of the yuan has come to an end. The future movement of the currency will be marked by more fluctuations.

However, even if Chinese authorities decide to depreciate the currency, the decrease will not be large.

Top policymakers' keenness for stability in the financial markets, as reflected in the unprecedented government intervention to try to reverse the recent stock market rout means that any appreciation of the yuan will be incremental and small.

In addition, given China's firm determination on yuan internationalization and its efforts to have the renminbi join the dollar, the yen, the euro and sterling in the IMF's Special Drawing Right basket, top policymakers will be unwilling to see the yuan drop to an extent that undermines the currency's popularity and use in overseas markets.

That is why the State Council has recently indicated that the trading band for the yuan will continue to be widened despite doubts over financial deregulation triggered by recent stock market woes.

The author is a Shanghai-based financial analyst. The views do not necessarily reflect those of China Daily.

(China Daily Africa Weekly 08/21/2015 page10)

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()