Africa has become a huge magnet for foreign direct investment as a result of uninterrupted economic growth by big African countries for more than 10 years. In that time, the continent's GDP has grown about 6 percent a year on average.

Foreign direct investment, commonly referred to as FDI, is an investment made to directly acquire lasting or long-term interest in enterprises located outside the economy of the investor.

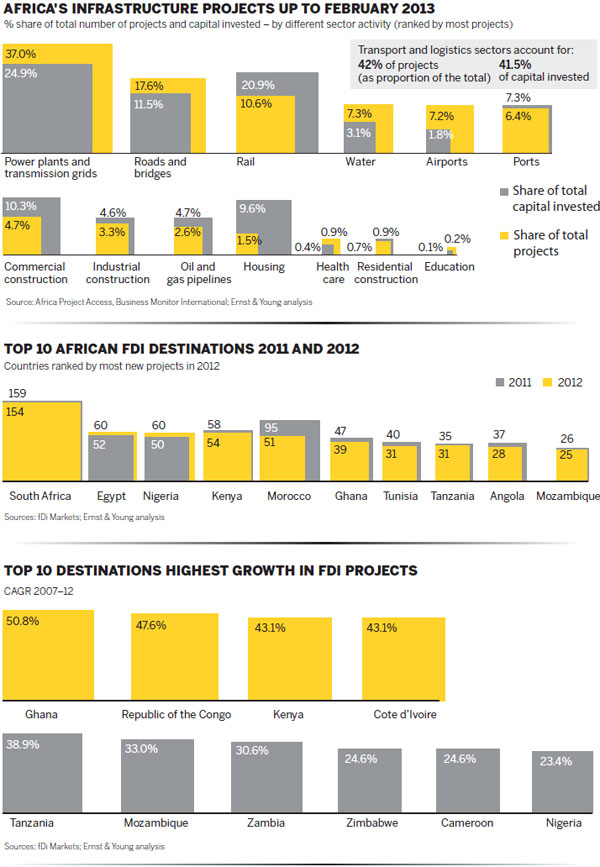

Africa's share of FDI inflows has significantly risen because of large projects, improved governance and infrastructure. Ernst & Young, the global consulting firm, says the value of infrastructure projects in different sectors of Africa exceeded $700 billion in 2012.

China has been a major player. Chinese firms have invested in key sectors such as telecommunications, transport, construction, power plants, waste disposal and port refurbishment.

"Given the scale of Africa's infrastructure deficit, these investments represent a vital contribution to the continent's development," wrote Harry Broadman, chief economist at PricewaterhouseCoopers in a report last year.

Burgeoning interest is found in many countries, he says. Chinese investors are engaged in building a $600 million hydro-electric plant in Zambia, and are investing in tourism in South Africa and Botswana. Huawei, the telecommunications giant, has won contracts worth more than $400 million to provide mobile phone services in Kenya, Nigeria and Zimbabwe.

Chinese firms also continue to build roads, railways, ports and government buildings. This is an extension of an early relationship under which the Chinese government gave modern infrastructure investment as gifts to African governments. This early engagement changed the face of infrastructure and made these countries more attractive to foreign investors.

Global FDI has increasingly been directed toward projects in Ghana, Kenya, Mauritius, Nigeria, Mozambique, South Africa and Tanzania. This has come even as investment in North Africa has fallen because of political upheaval.

FDI is no longer centrally focused on oil and minerals, and investors are diversifying into consumer sectors, recognizing the rise of the consumer class.

In West Africa, Nigeria, now the biggest economy in Africa, has surpassed South Africa after a recent rebasing of GDP, also known as statistical reassessment of its economy. Nigeria has managed to shake off its reliance on oil and diversified to become a service-based economy. The exercise captured industries previously either unaccounted or under-represented, such as information and communications technology, filmmaking and music, airlines, hospitality, online sales, and banking and finance.

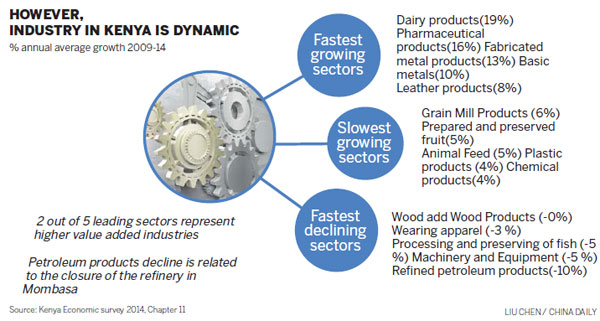

Competition from East Africa, in particular Kenya, has intensified. For a long time, the country's FDI inflows were dismal compared with its East African neighbors. Ugandan and Tanzanian inflows were directed to oil and natural gas industries, and Rwanda's sound FDI policies have given a huge fillip to the country's growth, particularly in information and communications technology.

Kenyan growth has been hampered by poor infrastructure, weak corporate governance, poor supportive structures to private organizations, weak FDI policy, a dearth of skills, a scarcity of known natural resources and the high cost of doing business.

However, it has enjoyed other competitive advantages, one being that the biggest economy in eastern and central Africa is strategically located. It is the gateway to the huge East African Community and common eastern and southern African regional markets, making it a beneficiary of several preferential trade arrangements.

As a result of the recent rebasing in GDP, the country has attained middle-income status, making it the ninth-largest economy in the continent, surpassing Ghana, Tunisia and Ethiopia.

Kenya's revised growth rate last year was 5.7 percent, significantly above an earlier estimate of 4.7 percent. FDI almost doubled to $514 million during the year.

The country has a new government keen on increasing FDI inflows. Double-digit growth of FDI by 2012, as stated in an ambitious economic blue print, failed to materialize.

Among economic reforms that have been implemented are reduced entry barriers to new businesses, privatization and attractive public-private partnerships. Heavy investment has also gone into improving energy reliability and distribution.

Last month the government, through its investment promotion arm, Kenya Investment Authority, held a two-day forum for investors in Nairobi. Those attending were told of the lucrative investment opportunities as well as government reforms to create an attractive investment environment.

During the event the government said it would increase the operations of the one-stop shop that KenInvest offers. President Uhuru Kenyatta directed the deployment to the center of 50 senior government officials with sufficient authority to make decisions.

"This will hasten the approval process," says Moses Ikiara, managing director of KenInvest. That process now takes 30 days, the World Bank says.

Fifty-nine government-approved projects were also promoted. The government says it plans to develop 10,000 kilometers of roads in less than five years, and most of the projects were related to power and transport infrastructure.

In addition, Kenya has fully liberalized its economy and removed obstacles that previously hampered the free flow of trade and private investment, such as exchange controls, import and export licensing and restrictions on remittances of profits and dividends.

Kenya is also working on expanding its international taxation treaties on double taxation agreements. This is important because they help in alleviating double taxation where business is conducted in different jurisdictions and also helps reduce the chances of tax evasion and helps in detecting it.

"There is no better time to invest than now," Ikiara says.

Despite the Kenyan government's optimism, gaps still exist that hinder the speed at which FDI inflows are absorbed. These relate to a shortage of skills, the number of bankable projects and the fragmented regional market.

The skills shortage is a huge constraint on growth. Despite having a highly educated workforce, with 55 percent estimated to be aged between 15 and 64, most lack market-oriented skills. For the country to achieve its development blueprint Vision 2030, it needs to have at least 7,500 engineers, 22,500 technologists, 90,000 technicians and about 450,000 artisans. Kenya only has 6,000 registered engineers, and there are no technologists.

There are 23 legally recognized universities in the country. The number of graduates is low because of limited admission, high costs of tuition and inadequate resources. Amid recent moves by these institutions to increase capacity, employers have complained that the graduates now being produced are ill prepared to meet labor market demands.

The Kenya Association of Manufacturers says the increased uptake of university education, especially in the humanities, means fewer people are being taught middle-level technical and manual skills that are needed to drive industry. A government program called Technical Industrial Vocational and Entrepreneurship Training is aimed at bridging this gap.

However, the World Bank says the system suffers from critical problems, including a decline in the quality of training, a lack of relevance to occupational and social realities, a lack of enrollment and a lack of funds.

In addition, the government lacks the technical capacity to negotiate mutually beneficial alliances with the private sector. Previous partnerships have had minimal impact and some heavily indebted projects have collapsed. Export processing zones have also failed to diversify the country's industrial base because most of the beneficiaries are textile firms targeting the US market.

This has affected the way the government designs and delivers information to investors. So opportunities are lost as investors carry out due diligence before committing funds. The situation has nurtured intermediaries who have made matters even more complex.

Sino-Africa Future Corporation Limited, an advisory firm that links Chinese investors to Africa, says that accessing technical and market information is a challenge at the national and county levels in Kenya as there is no handbook detailing projects, their scope and value and model of entry.

The agency, set up in September this year, managed to bring 70 Chinese delegates to the investment forum in Nairobi last month, an indication of strong Chinese interest in the market.

"Investors weigh their risks and returns together with other dynamics to inform their decisions," says Eric Hou, the company's business associate. Most business ventures fail partly due to poor selection, while 80 percent fail due to weak cultural synergies, he says.

Christian Li, director of business consulting for the investment firm China House, has been in Kenya for six months. The firm, which is primarily interested in the energy sector, has entered the Ethiopian market, too.

In a program known as Subcontracting and Business Partnership Exchange, an initiative of the United Nations Industrial Development Organisation and KenInvest, 120 local small and micro enterprises were profiled between 2010 and 2011 but only six have been successfully linked up.

The program's aim is to fast track industrialization processes in less developed countries by mainstreaming SMEs into a global value chain of services and manufacturing.

"The program is good for SMEs but there was poor marketing," says Ken Manyala, an economist who has previously consulted for International Finance Corporation, a World Bank agency under the IFC-East Africa Community Investment Climate program. Businesses are unaware of the program, and the promotion agency is severely underfunded, he says.

By taking a close look at local companies it was hoped to gauge their ability to plug into a high value chain, but their productivity levels failed to satisfy multinationals' demands.

Manyala says little has been done in developing special economic zones which are successful in North African countries, such as Egypt.

"There is high private investor demand for these zones because of the free land and attractive incentives, elements that directly affect the bottom line."

Land is a very sensitive issue in Kenya, and its management and tenure system affects investment. There is an impasse between the government and landowners in cases where land has been taken to develop big infrastructure projects, and this is sending the wrong signal, Manyala says.

Another problem is that the process of integrating regional markets is painfully slow. At the moment tariff and non-tariff barriers continue to make intra-continental trade expensive. The monetary systems remain fragmented, and common market agreements are yet to be fully implemented.

However, there is reason for optimism. Experts are now calling for a more regional approach, especially in infrastructure development agreements. This comes as China plays a leading role in infrastructure development. The country has contributed $3.8 billion toward a railway project linking Kenya, Uganda, Rwanda and South Sudan.

Policies should be developed that offer professionals lucrative employment opportunities and attract citizens abroad to return home, says the economist. An estimated 20,000 African professionals have emigrated from the continent every year since 1990.

Officials say that capacity building should also be a joint venture between the public and private sector. Considering the limited resources and skills of the Kenyan government, the private sector can help it overcome capacity gaps particularly in finance and trade.

"Counties need to be trained in the public budget building process, expenditure and also creating a good investment climate to attract FDIs," Manyala says.

Investment promotion boards need to be established and be well funded to effectively carry out their mandates, he says. Local governments have also been viewed as amiable partners as they exude passion and excitement when dealing with foreign investors. But Machakos county in Kenya is the only one with a promotion agency.

To increase counties' attractiveness, the Kenyan government needs more regulatory reform to increase transparency in processes such as procurement. This will increase the level of uptake for public-private partnership projects.

Funding to learning institutions needs to be increased, especially in the research and development departments, which will sharpen negotiating and execution skills in investment projects, Manyala says.

"The PPP is a new concept and still under research. The projects being identified need to be well thought out so the results increase the level of investor uptake."

The move will also strengthen the link between academia and business communities, says Nicholas Onditi, vice-chairman of the Kenya National Chamber of Commerce and Industry.

Education would be solution based, and graduates would have relevant market skills.

"There is no meaningful growth without research and development," says the vice-chairman.

The recently revamped national chamber intends to increase local content or participation by mobilizing and supporting rural-based enterprises where households venture into business. Credit facilities will also be provided to capitalize these ventures, with the chamber being the guarantor.

"We want to create a bottom-up economy," Onditi says.

By encouraging the growth of rural enterprises and not focusing on the urban industrial sector, Kenya will successfully move workers into factories while mitigating against urban crisis. Subsequently local content would enable partnerships.

"FDI should not be geared toward increasing employment but technology transfer," says Vimal Shah, an industrialist, and chairman of Kenya Private Sector Alliance.

The relatively good workers in Kenya have "fire in their bellies" and only need opportunities to sharpen their skills, he says, and more bankable projects will emerge.

"Kenya is a work in progress."

Comprehensive market reforms will also result in the financial sector broadening its credit products to increase borrowers. The country would achieve faster growth if many SMEs had access to capital. Recently launched credit referencing by banks has been received skeptically because the number of borrowers is low and those who save are fewer.

Financial literacy programs are encouraged and even integrated into Kenyan school programs. The country needs to shore up local investment levels to 30 percent of GDP from the 15 percent recorded in 2011, says Shah.

The threats to security and of corruption are hampering the country's prospects. Government funding to address security issues has been increased in the 2014-15 national budget.

lucymorangi@chinadaily.com.cn

|

Delegates share in a lively discussion before the opening of the forum. Photos By Xie Songxin / China Daily |

|

A Chinese representative talks with an African counterpart in a forum. About 70 Chinese delegates attended Kenya's first international investment conference, which was opened by President Uhuru Kenyatta in Nairobi last month. |

|

Kenyan President Uhuru Kenyatta shares a light moment with Ambassador Richard Sezibera, secretary-general of East African Community, during the opening of the Kenya International Investment Conference in Nairobi last month. Xie Songxin / China Daily |

(China Daily Africa Weekly 12/05/2014 page6)

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()