Chinese companies use sustainable development to chart a new course in Africa

At first glance, it is hard to find something in common between the Tonkolili and Palabora mining projects in western and southern Africa. While the former is engaged in iron ore extraction, the latter is primarily a copper producer.

But what links these two diverse projects is the Chinese investment that has provided the much-needed funds for the big-ticket projects that have long-term implications for the African economy.

Though China has a rich trading legacy with Africa, its outbound investment moves on the continent have been relatively modest till now. That looks set to change, as a host of Chinese state-owned and private enterprises are actively pursuing M&A opportunities across Africa in countries such as Nigeria, Sudan, South Africa, Uganda, Kenya, Sierra Leone and Egypt.

Though much of the activity is resource-driven, it is slowly percolating down to other sectors such as appliances and financial services. What makes these outbound moves interesting is the unique approach adopted by Chinese enterprises to provide funding, technology and jobs.

Sustainable development and well-being of local communities are the new growth drivers for Chinese companies in Africa rather than just profits, experts say.

"As the Chinese economy develops and becomes the world's economic motor, it's inevitable that more Chinese companies will spread wings in Africa," says Yao Shujie, head of the School of Contemporary Chinese Studies at the University of Nottingham in Britain.

The most visible face of Chinese engagement in Africa is the Tonkolili iron ore mine in Sierra Leone. Spread over 30 kilometers in the hills around Bumbuna, Mabonto and Bendugu in the Western African nation, Tonkolili, operated by the AIM-listed African Minerals, is the biggest iron ore deposit in Africa and the third-largest in the world.

Last month, Tianjin Materials and Equipment Group Corporation, China's largest iron ore import and export enterprise, agreed to invest $990 million in the more than $6 billion iron ore project.

Under the terms of the deal, the Chinese company would receive a 16.5 percent economic interest in the Tonkolili project in exchange for its almost $1 billion investment.

According to the "strategic, binding" memorandum of understanding, the two sides also have a 20-year offtake agreement and the creation of a joint venture to blend and market iron ore through the major Tianjin port facilities.

African Minerals, one of several developers betting on West Africa's potential to become a major supplier of iron ore, has indicated that the Chinese investment would be made in two stages. First, the Chinese company would buy new shares in African Minerals for $390 million, amounting to a 10 percent stake in the company. African Minerals will then sell the Chinese company a 10 percent stake in the iron ore project for $600 million.

The 20-year offtake agreement is for a total of 10 million tons per year of iron ore, or proportionately less if the capacity of the project's second phase expansion is less than 35 million tons per year.

In August, Hebei Iron and Steel Group Co, China's largest steelmaker, acquired a 74.5 percent stake in a South African copper mining company. Upon completion of the transaction, Hebei Iron will operate and manage copper miner Palabora Mining Company Ltd as its largest shareholder. The agreement was signed in December last year between a consortium led by HBIS and Anglo-Australian mining giant Rio Tinto in Beijing.

According to the agreement, the consortium and South Africa's Industrial Development Corp will jointly purchase the 74.5 percent stake in Palabora held by Rio Tinto and Anglo American Plc for $493 million.

Founded in June 2008 through the merger of Tangsteel and Hansteel, both located in North China's Hebei province, Hebei Iron had assets worth 316.8 billion yuan ($51.1 billion) by the end of last year with that year's steel output reaching 42.84 million tons. It is also the world's second-largest steelmaker after ArcelorMittal.

Yao from the University of Nottingham, who has worked in Africa for more than seven years, says the changing global economic situation and the financial crisis in the eurozone have prompted major economies such as China, the United Kingdom and France to shift their investment focus from traditional markets in Europe and Asia to Africa.

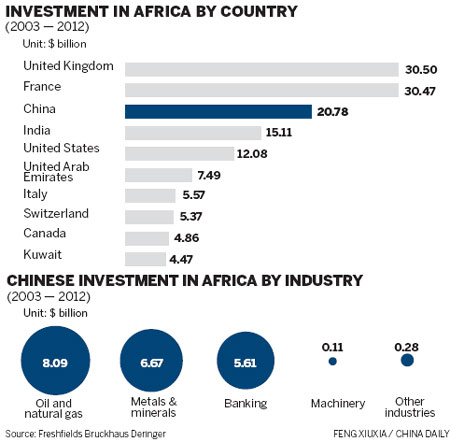

In July, international law firm Freshfields Bruckhaus Deringer released a report that stated that China has become the world's third-largest country doing mergers and acquisitions in Africa, especially in the oil and gas sector.

Chinese enterprises have conducted 49 M&A deals totaling $20.78 billion in Africa since 2003, following the United Kingdom with $30.5 billion and France with $30.47 billion.

Most of the Chinese deals were in the natural resources sector with $8.1 billion invested in oil and gas across three deals and $6.7 billion invested across 19 deals in metals and mining over the past 10 years. The Chinese preference for these sectors is likely to continue in the long term, the report said.

Globally, 1,190 M&A deals totaling $87.6 billion were done in Africa over the same period. South Africa, Nigeria and Uganda are becoming active M&A destinations for Chinese investors with 23 deals totaling $16.4 billion to date, said the report.

One of the largest Chinese deals in Africa has been the China-Africa Development Fund's acquisition of a stake in Misr Refrigeration and Air Conditioning Manufacturing Co, a Cairo-based manufacturer of refrigerators and air conditioning systems, from the Barakat Group, for $5.6 billion in 2010.

The value of African inward investment has tripled in the past 10 years reaching more than $182 billion, up 214 percent in 2012 compared with 2003.

Yao says that China's acquisitions in Africa are based on mutual benefits. For China, the acquisitions will help companies to reduce the trade costs and develop overseas markets. Africa is also rich in resources and low-cost labor. For African countries, the Chinese deals have helped upgrade the continent's technological, managerial and competitive abilities.

"Chinese investments have also proved beneficial for further development, jobs and urbanization," Yao says, adding that Chinese companies have provided solutions for tackling poor levels of infrastructure, high unemployment and poverty in Africa.

China-Africa trade stood at nearly $200 billion last year, with Chinese investment in Africa moving up to $17 billion, according to the department of African affairs at the Ministry of Foreign Affairs.

Seth Rosenfeld, an analyst at investment banking firm Jefferies, says that though the outlook for funding new mine developments has become increasingly difficult in the past few years, the Tonkolili investment should leave African Minerals well placed to push ahead with its expansion plans.

"Together with $502 million of cash on hand at the end of the first half ... and with strong cash flow generation from current operations, we estimate that African Minerals could end this year with around $1.5 billion," Rosenfeld said in a research note.

Jobs benefit

While some Chinese employers in Africa have been criticized for their failure to transfer skills or provide many job opportunities to local people, several other Chinese companies have made great progress in Africa in recent years in these areas.

Benson Wakhanu Mwanyande, who has been working for China Road-Bridge Co in Kenya for more than 15 years, says that Chinese companies offer more opportunities to learn skills.

"Unlike the other projects that I have worked with, the Chinese projects offer freedom and flexibility and also opportunities for work rotation to gain well-rounded knowledge," he says.

According to China's Foreign Ministry, Chinese companies in Africa have to date created more than 350,000 job opportunities.

Zheng Yuewen, chairman of the China-Africa Business Council, which represents the interests of more than 550 Chinese companies in Africa, says that revenue from Africa has been the mainstay for most of its members. Last year, the CABC conducted a survey among 198 member companies to gauge the contribution of Africa.

With 34,000 local employees and 6,400 Chinese workers, these companies had trade relations with 51 African countries and $2.4 billion in sales revenue last year, representing about 16 percent of their total business revenues.

The 198 companies, including the Chongqing-based automobile producer Lifan Group, Guangdong-based shoemaker Huajian Group and power supplier Shenzhen Energy Corporation, have so far invested $1.1 billion in 32 African countries and have plans to invest an additional $5 billion over the next three years.

Around 80 percent of CABC's members are private companies, while the rest are state-owned enterprises. Notable deals include home appliance firm Midea's $58 million stake in Egypt's Misr Refrigeration.

Vital difference

Yao from the University of Nottingham feels that China's acquisitions in Africa are different from those in Europe, where the focus is invariably on gaining advanced technical know-how.

Germany is still the top choice for M&A deals by Chinese companies due to its wealth of engineering talent and premium technology.

Last year, Chinese companies snapped up German industrial giants such as forklift maker Kion Group and cement-machinery maker Putzmeister. Other destinations such as the UK, Italy, Switzerland and France are also seeing more interest from Chinese companies, such as Bright Foods' acquisition of British breakfast-cereal brand Weetabix.

According to data provided by stock market research firm Dealogic, the value of Chinese acquisitions in Europe reached $10.5 billion (7.8 billion euros) in 2012, compared with $259 million in 2002. The number of Chinese deals in Europe in 2012 reached 78, compared to just 11 in 2010, according to Dealogic.

China Investment Corp, the country's sovereign wealth fund, acquired minority stakes in infrastructure such as Heathrow Airport Holdings and Thames Water in the UK. Another state-owned company, China Three Gorges Corp, bought 21 percent of Portuguese power company EDP-Energias de Portugal SA.

Experts expect the M&A trend will continue, as Chinese companies, finding growth slowing at home, are increasingly looking abroad for foreign markets and strong brands.

"In the future, China will invest more in Africa, Latin America and Asia, especially in developing countries," Yao says, adding that China has comparative advantages in such areas.

"The scale and pace of acquisitions by Chinese companies across the African continent will pick up substantially."

Marcus Shadbolt, a partner at the China-focused financial advisory firm Vermilion, says, "Going forward, I expect there will be a continuation of investment in Africa and this will extend from natural resources and physical infrastructure into other supporting sectors, such as financial services and some consumer businesses, as economies like South Africa, Egypt, Nigeria and Morocco are becoming more important in the global context".

"Smart partnership deals with foreign companies will also become more prevalent, as a means of leveraging respective synergies and managing risk, especially political risks."

Contact the writers at cecily.liu@chinadaily.com.cn and zhang chunyan@chinadaily.com.cn

Wang Mengzhen contributed to the story.

|

People work on the assembly line at a Huajian shoe factory in Dukem, Ethiopia. The Guangdong-based company is one of the major investors in the country. Jenny Vaughan / AFP |

|

Above: Zheng Yuewen, chairman of the China-Africa Business Council. Below: Yao Shujie, head of the School of Contemporary Chinese Studies at the University of Nottingham in Britain. Photos Provided to China Daily |

( China Daily Africa Weekly 10/11/2013 page1)

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()