Realities of risk

Debt levels in China have become a major focus for policymakers, but experts don't always agree

Is China facing a debt bubble?

Housing prices have soared by more than 30 percent in many of the country's tier-one cities, such as Beijing and Shanghai this year alone.

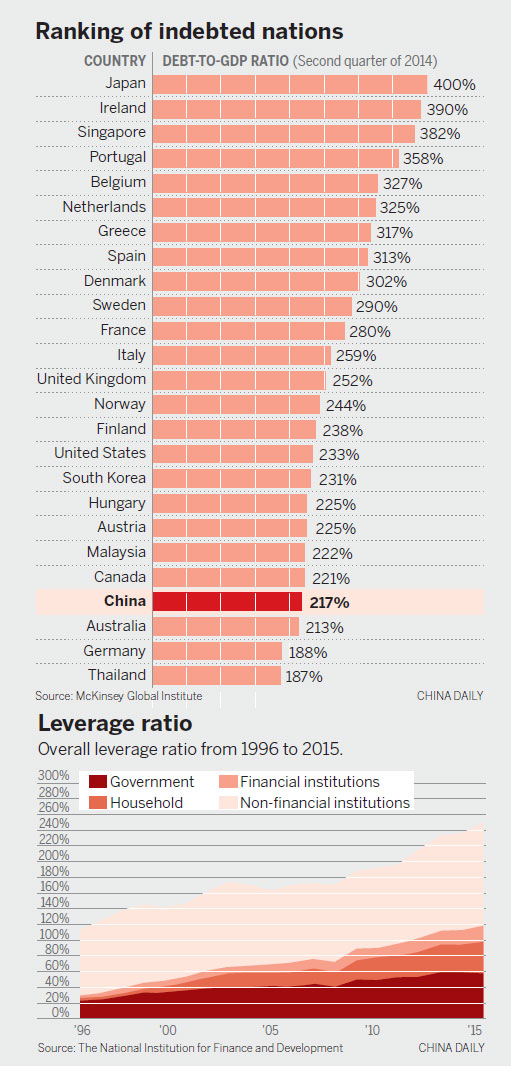

Research by the National Institution for Finance & Development, one of China's national-level think tanks and part of the Chinese Academy of Social Sciences, put China's debt at 249 percent of GDP in 2015.

A new book, China's Guaranteed Bubble, by Zhu Ning, professor of finance at Tsinghua University, makes the argument that many Chinese do not properly understand risk.

It says there is now a dangerous culture emerging in China of people regarding investing in property and other assets is a one-way bet and that if anything goes wrong the government will bail them out.

Levels of debt in China have become a major focus for policymakers.

There have also been recent concerns about a credit crunch happening sometime before Chinese New Year, as was the case in the runup to the festival in 2013.

This has been reflected in higher bond yields, with 10 out of 19 banks and brokerages in a Bloomberg survey saying that 10-year sovereign yields will rise to 3 percent by the end of the year.

The government recently made clear its commitment to controlling debt. It announced strict guidelines on Nov 14 to strengthen budget management at the local government level.

However, according to one of the latest major international comparisons of debt by the McKinsey Global Institute for the second quarter in 2014, China did not particularly stand out.

Its debt level then was 217 percent of GDP, ranking it 22nd among indebted nations, well behind Japan which had the highest ratio, 400 percent. France was 280 percent, the United Kingdom 252 percent and the United States 233 percent.

Andrew Leung, founder of Andrew Leung International Consultants and a leading China commentator, says a lot of the discussion about China's debt underestimates the strength of the country's assets.

"You can't just look at debt. You have to look at debt and equity. If people borrow money to buy a house, they have the asset of a house. A lot of China's assets are worth serious money."

The main concern is the speed at which China's debt has risen. According to Bloomberg Intelligence, it grew 465 percent in the decade up to 2015, with corporate debt (mainly that of state-owned enterprises) increasing from 105 to 165 percent of GDP.

Fred Hu, chairman of China-based global investment firm Primavera Group and former greater China chairman for Goldman Sachs, says China is still dealing with the consequences of the 4 trillion yuan ($580 billion; 550 billion euros; 470 billion) stimulus that was injected into the economy after the global financial crisis in 2009.

"The debt has exploded to a very high level within just five to six years. History has shown that episodes of fast credit expansion inevitably lead to misallocation, rising nonperforming loans, banking sector stress and ultimately a financial crisis," Hu says.

Louis Kuijs, head of the Asia section at Oxford Economics, based in Hong Kong, believes rising debt is a serious issue but considers a financial crisis unlikely because the banks have a healthy deposit base.

"I do not think that a systemic financial crisis is likely anytime soon because the bulk of the debt is owed domestically and the financial system is still very liquid, with a loan-to-deposit ratio well below 100 percent, unlike in any typical country that has fallen into a financial crisis in recent decades," Kuijs says.

Leung says this is an advantage that China has over the United States and many European countries: Almost all of its debts are owed internally within its own financial system.

"There is very little external debt," Leung says. "In this case China is very similar to Japan, and very different to most Western countries." Japan also has a savings culture and strong deposit base.

Duncan Innes-Ker, regional director for Asia at The Economist Intelligence Unit in London, also believes having little external debt eases the pressure on China.

"It is certainly a positive, although running up domestic debts is not cost-free, as it tends to put downward pressure on the currency and will add strains in the banking sector," he says.

"However, policymakers have more control over the situation than they would have if debts were owed abroad. China's high domestic savings rate makes it easier to borrow domestically, so that is another advantage it has."

One of the main arguments in the book by Zhu, the Tsinghua professor, is that investments in China often appear to have some sort of implicit guarantee from the government, thereby creating irrational behavior.

He says wealth management products offered by banks and other financial institutions sometimes offer 20 percent returns while claiming there is no risk to capital.

Michael Pettis, professor of finance at Beijing University's Guanghua School of Management, believes it is a "moral hazard" question that needs to be addressed in China.

"It is what we call the process by which profits are retained by investors and all or a significant proportion of the losses are passed on to some other entity like the government," he says.

"It creates a systemic tendency to overinvest or to invest in excessively risky projects, because it eliminates most of the downside for investors by passing losses on to the government. I wouldn't say Chinese investors have no understanding of risk. On the contrary they understand very well and are taking advantage."

Jeremy Stevens, Beijing-based China economist at Standard Bank, Africa's largest bank, believes the government is beginning to tackle the problem.

"We are seeing a more serious approach from the government, and it is beginning to allow defaults and bankruptcies and provide the institutional framework in which bankruptcies can be undertaken. This change has been incremental and probably not bold enough quite yet," he says.

For many, the most concerning potential bubble in China is the housing market, where prices have been soaring in tier-one cities. Beijing and Shanghai now boast some of the highest house prices in the world, although the country itself has a long way to go to achieve high-income status.

George Magnus, senior independent economist at UBS in London, says there are parallels between China and many Western countries in the runup to the financial crisis in the last decade.

"There was an assumption that property prices would continue rising. The Western credit bubble was built around the idea of home ownership in Britain and the US, and in Spain and Ireland, although it was not a typical continental (European) problem."

Pettis, also author of Avoiding The Fall: China's Economic Restructuring, believes the housing price boom may have some way to go before it becomes a bust.

"An unsustainable rise in real estate prices can persist for much longer than economists expect," he says.

"Before they fell in the early 1990s, for example, Japanese real estate process probably exceeded fair value by at least twice as much as Chinese real estate prices do today."

Stevens at Standard Bank says financial crises always tend to result from the liabilities side of the balance sheet rather than on the assets.

"So far, the government has been resolving tension in the system by focusing on the assets side and pushing through excess capacity cuts on the supply side of the economy and introducing curbs to prevent speculation on the housing market," he says.

"What is happening on the funding side is more up for debate. The problem is that you need credit growth in the economy to decelerate."

Some observers believe the Chinese government needs to move away from its target to double its 2010 GDP by 2020 if it expects to break out of the middle-income trap and become a high-income economy.

To meet this target it needs to achieve 6.5 percent growth every year. This year growth, has been 6.7 percent in each of the first three quarters.

Pettis estimates that in achieving the goal this year alone, debt rose 15 to 20 percent.

"Only after Beijing gives up its growth target, as it must, will it be able to control the growth in its debt."

Leung says the way China's financial system operates gives it great resilience with loans from state-owned banks being recycled back into the system as deposits. Corporate deposit holdings in China are around 90 percent of GDP, compared with 7 percent in the US.

"China has an exceptionally high level of corporate deposit holdings. As loans are often recycled back to the lending bank as deposits, that enables the banks to earn high interest spreads, and it acts as a cushion against any exigencies," he adds.

Magnus, also an associate at the Oxford University China Centre, believes China's economic leadership, including the National Development and Reform Commission and the People's Bank of China, are fully aware of what they have to do, but it is a major challenge.

"These are smart people who think very carefully about problems," Magnus says. "They may not always have the implementation capacity but they think very cleverly about what is going on."

andrewmoody@chinadaily.com.cn

|

Jeremy Stevens, China economist at Standard Bank, Africa's largest bank, believes the China government is beginning to tackle the debt problem. Zou Hong / China Daily |

( China Daily Africa Weekly 11/25/2016 page1)