IPO arrow on regulator's bowstring

Reforms herald breakthroughs like domestic floats of tech unicorns and overseas-listed Chinese companies

When the Shenzhen Stock Exchange launched the ChiNext board in 2009, Beijing had hoped it would someday grow up into China's Nasdaq and be home to stocks of the country's most valuable innovative startups and a cradle of future Chinese tech equivalents of Apple and Microsoft.

Nine years on, the board seems to have fallen short of such expectations.

That state may have been due to companies such as Leshi Internet Information & Technology Corp. The videostreaming firm was once touted as one of the most promising startups. Some even called it the brightest tech star of ChiNext. But alas, Leshi turned out to be a scandal-ridden, financially troubled company.

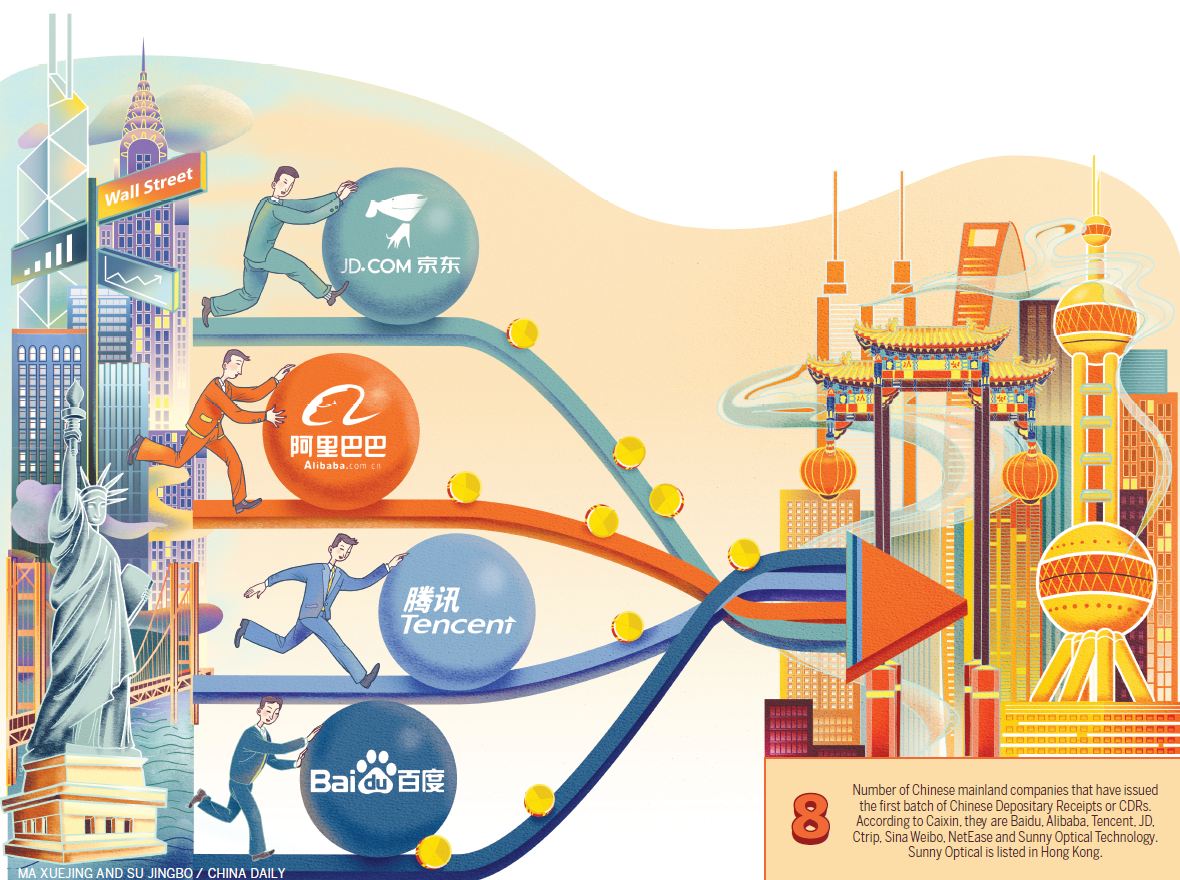

What added to ChiNext's embarrassment is the fact that the country's most well-known tech giants-Baidu, Alibaba, Tencent and JD, which are abbreviated as BATJ-have all listed their shares on overseas markets.

Hundreds of millions of users in China use BATJ's services on a daily basis. Yet they have either very limited means or almost no way to buy shares of BATJ. In contrast, the Big Tech Four offer prodigious returns to overseas investors who are not exactly its consumers/users.

For instance, Alibaba Group Holding Ltd, whose world record-breaking initial public offering on the New York Stock Exchange raised $25 billion in September 2014, offered its shares at $68 apiece. The stock started trading at $92.70 straightaway.

Nearly four years after the IPO, Alibaba's stock price has increased by more than 190 percent.

What about investors in China where Alibaba earns most of its revenues and profits? "Many good companies are developing and the domestic (investors) have not been able to enjoy the fruits and profits of their development. This is a historical regret. Entering the new era, this regret should no longer continue," said Liu Shiyu, chairman of the China Securities Regulatory Commission, while interacting with reporters on the sidelines of the two sessions, the annual meetings of China's top legislature and political advisory body.

Such regrets have prompted the CSRC to ponder significant regulatory changes. It now aims to not only bolster the Shanghai and Shenzhen stock exchanges' status as attractive listing hubs for technology firms but catch the next wave of IPOs by Chinese "unicorns" (those with a valuation of $1 billion or more each).

The securities regulator's move to boost tech representation in the stock markets is in line with the country's transition toward higher-quality economic growth driven by innovation and technological advancement.

Just as Chinese President Xi Jinping has pointed out, China is in a critical period of improving its economic structure and upgrading the growth engines of the economy.

Beijing hopes the capital market will play a bigger role in nurturing the new economy and serve the financing needs of small but promising companies.

To realize such hopes, the CSRC has started to fast-track the approval process for tech IPOs. The latest evidence was the superfast approval for the planned $4.3 billion IPO by Foxconn Industrial Internet, the local unit of the world's biggest contract manufacturer.

Foxconn's clients include Apple and Amazon. In a record-breaking 36 days, Foxconn received the CSRC's green signal. Normally, it could take months or even years for companies to obtain the regulatory go-ahead for IPOs.

In addition to speedy approvals, the regulator is reportedly considering according "special treatment" to unicorns. This could mean easing of the profitability requirement for IPOs of unicorns from the four sectors of biotechnology, cloud computing, artificial intelligence and advanced manufacturing.

The Shanghai and Shenzhen stock exchanges are also drafting detailed rules and arrangements that will allow overseas-listed Chinese tech companies to return to the home markets.

The idea is to make amends for the "regret" and enable mainland investors to trade their shares.

Encouragingly, executives of tech companies including Baidu Inc and NetEase Inc have expressed interest in listing their shares on domestic stock markets as well.

Electronics and software company Xiaomi Corp is also said to have planned a float on both the Chinese mainland and Hong Kong markets.

Wang Jianjun, general manager of the Shenzhen Stock Exchange, said the bourse has finished the basic preparation for a pilot program that will allow listings of tech unicorns. He hoped the regulator would allow innovative firms that are not yet profitable to float shares in the domestic capital market.

Analysts said the anticipated domestic floats of overseas-listed tech companies and tech unicorns will require a major revamp of existing rules. Under the current IPO regime, requirements related to continuous profitability and share structure are considered very stringent.

For example, one listing requirement of the Shenzhen's startup board is that a company must be profitable in the past two years and have profit of at least 10 million yuan ($1.58 million) or have net asset of at least 20 million yuan in the previous quarter. Another example is that the law requires that a shareholding company must follow the "one share, one vote" principle.

"The existing rules were designed for the old industrial economy with too much emphasis on business scale and profitability. It would be very hard for the new unicorn companies to meet these requirements if the regulator does not make changes to the rules," said Dong Dengxin, a finance professor at the Wuhan University of Science and Technology.

Dong said the IPO reform also faces immense legal hurdles as the country's existing laws ban companies registered in overseas markets and those with dual-class share structure from selling shares in the mainland stock markets.

Dual-class share structure refers to the arrangement that grants a particular group of shareholders greater voting rights than others, different from the "one share, one vote" principle.

Media reports have suggested that the securities regulator is considering introduction of Chinese Depositary Receipts, a system that will allow overseas-listed companies to transfer part of their shares to a custodian bank, which can sell them on a mainland exchange board.

"We have studied the option of CDRs for a very long time and have made preparations in terms of trading system and rules. At present, the conditions have become relatively mature," Wang, the head of the Shenzhen bourse, was quoted by Shanghai Securities News as saying.

The priority the mainland regulator and stock exchanges are giving to tech companies also underscores the intensified competition among Asian bourses.

The Hong Kong stock exchange and the Singapore Exchange are expected to offer soon favorable terms for companies with dual-class share structure, in a bid to get ahead in the regional IPO race.

"The IPO reform of the mainland market is like an arrow on a bowstring. We can expect major breakthroughs," Dong said.

Equity analysts and market mavens are already wondering about the potential impact of the expected IPO deluge on the A-share market.

"Overseas-listed companies will have greater advantage as they are often higher-quality companies. They will get more attention from the investors if they list on the A-share market. And because investors have more options, their local listing could exert pressure on the prices of existing A shares," said Gao Ting, chief China strategist at UBS Securities.